Since we have been talking about our own portfolio in the previous emails specially aboutAxis Bank and Oriental Bank of Commerce where we had some terrific returns some members emailed us with lots of praises for our stock picking ability. So to prove that the praise is not justified and why we are not experts when it comes to stock picking, we will talk about one of our investment which we made couple of years back.

Persistent which specializes in IT products and services off shoring listed on NSE in April 2010 at around 400 Rs. Fast forward to June 2011 most of the world stock markets were spiralling downwards, the “experts” gave the usual reasons like inflation, Quantitative Easing, problems in middle east etc. Almost all Indian stocks got hammered but Persistent took a more significant hit. It crashed to around 290 Rs because “experts” believed that it wont be able to compete with the other IT biggies like TCS, Infosys, Wipro. So most of the brokerage houses gave a SELL recommendation. When others start selling that is the time we get active.

We quickly added Persistent to our database. What we saw was that Persistent was having good profit margins with Net Profit Margin above 15%, good ROE above 15%, positive free cash flow ( old members by now should know that we are big fans of companies with positive FCF), high current ratio, no debt, net income as well as Cash flow from operations positive with CFO higher than net income (which is a sign of good management), above 30% revenue growth in the last 5 years(2009 was an exception).

There was one drawback though, the company was issuing more shares, as we have said on the website, issuing more shares can be beneficial only if the company is able to increase shareholder value in the long run, most companies are not able to do that.

The valuation models gave a fair value around 425 Rs.

A quick look at the annual report and we did not find any negatives there. So Persistent was a fundamentally good company, selling cheap. There was really no justification for the claim that it would not be able to compete with companies like Wipro, TCS in the future when it was successfully competing for the last 5 years.

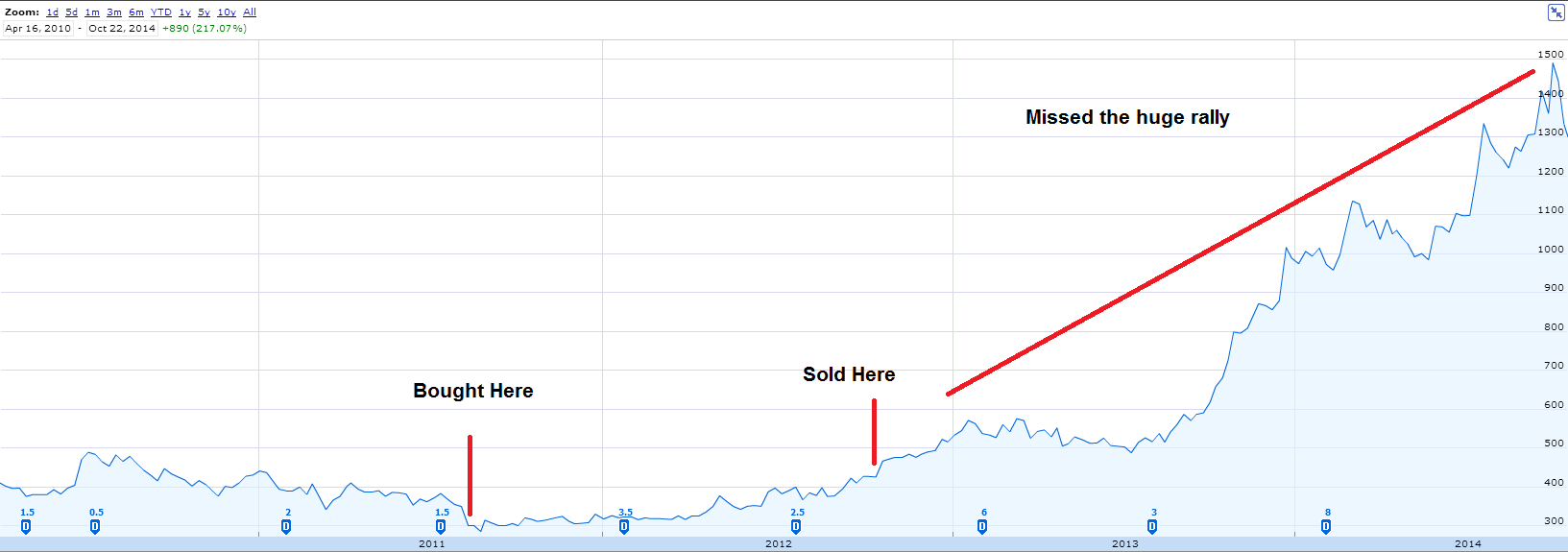

So we bought the stock at around 300 Rs. in Aug 2011 and we sold it in Sep 2012 around 425 Rs, the fair value at that time was 440 Rs as per the valuation models. A return of 42% in almost one year. We were quite satisfied with the return and invested the money in some other stock. So what was our spectacular mistake. Check Persistent’s current share price, its 1333 Rs. We would have made a spectacular return if we had not sold the stock. There was really no reason to sell the stock, we sold it just because the share price was near its fair value. The company was still doing great fundamentally.

What can you learn from this, dont sell shares of good companies. Dont sell just because the share price is near the fair value and dont sell because the “experts” on TV are shouting to sell. From 2011 till 2014 you must have heard all the bad news on TV like, problems in Ukraine, problems in US, problems in middle east but you can ignore all these news if you have invested in a good company.

A quick note to all the new members, we occasionally talk about our own portfolio to educate our members, please do not email/call us for investment advice. We do not provide investment advice.

I will right away seize your rss as I can’t find your email subscription hyperlink or newsletter service.

Do you have any? Kindly let me understand so that I may subscribe.

Thanks.

LikeLike