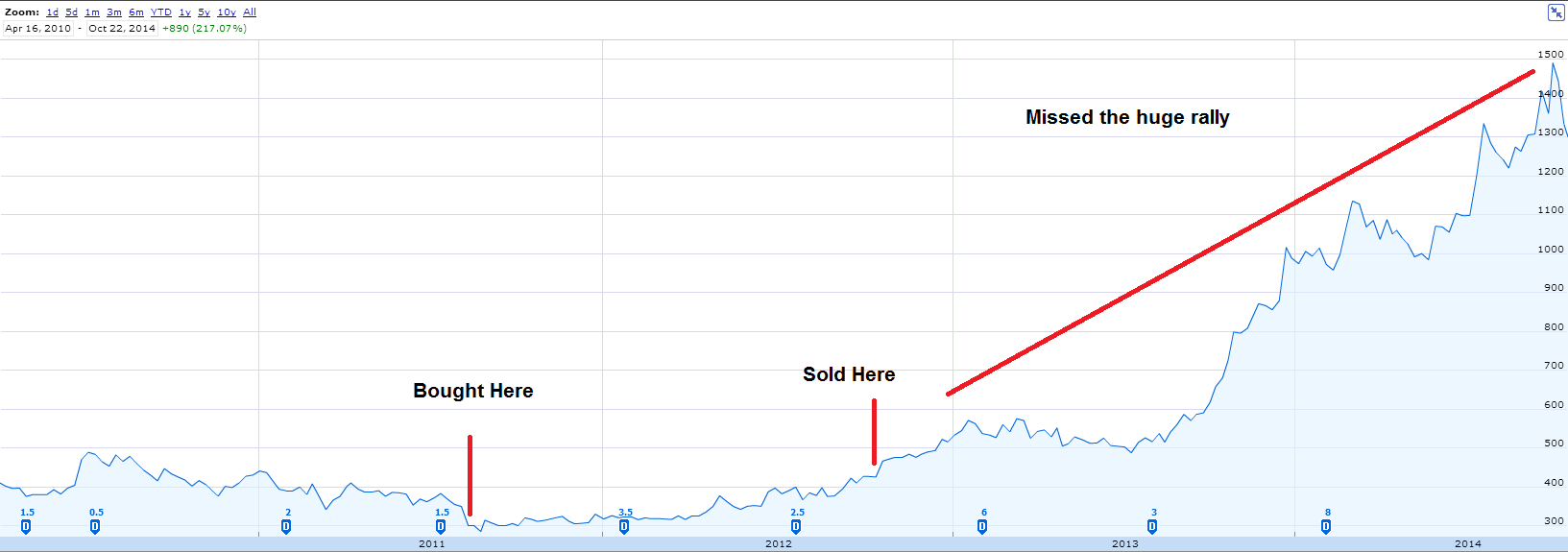

We wrote about Axis Bank back in Sep 2013 and Jan 2014 where we said that the whole stock market specially the banking sector was undervalued. We had purchased Axis Bank and Oriental Bank of Commerce for our own portfolio, we sold Oriental Bank with good profits because we were not comfortable holding it for long term.

As you can see in the image that we missed the short sharp rally after we sold our position but that is okay since we are not greedy. Look how the stock performed after the rally, the price dropped. So our decision to sell was infact right.

Coming back to the main topic of Axis Bank. We still have not sold our position but we do monitor it every now and then. Take a look at the Insider Trading activity for Axis. You can see that institutional investors like Life Insurance Corporation Of India, United Insurance have been selling the stock in huge quantities in the month of Jan 2015 and Feb 2015. We could not figure out why they were selling since we didnt think anything fundamentally had changed with the company. So we ignored those sell transactions and held our position.

Two days back LIC bought Axis Bank shares again and we suspect they will buy more in the coming weeks. So we ask the question to our readers, do you know why LIC dumped the shares two months back and started buying again. We think LIC made a mistake in selling Axis shares, even they realized the mistake and so started buying the stock again. Axis is a good bank to invest for long term.

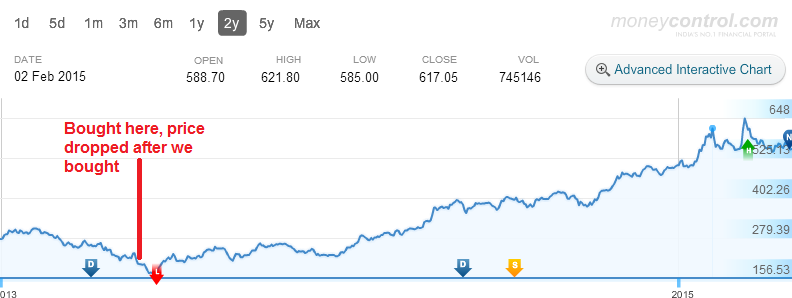

Axis Bank Stock Performance, note the price drop after we bought. Intelligent investors should not panic if the price drops after you buy the shares. If your analysis about the company is right, the price would rise again, slowly but surely.