We recently added ACC to our database. When we add any new company to the database we avoid looking at the share price. We add the data and then look at the performance, growth pages and then make a decision whether it is a good company to invest or not.

If you look at the profit margins and ROE charts you will immediately see that all of them are dropping down consistently for many years. Most of members do check these charts but we have seen from our website logs that most members don’t look at the Growth page. So we just want to point out how the Growth page can help you make the decision.

The above information tells you that ACC does not have a good Revenue growth for all these years. The next two lines tell you (this is very crucial) that all the sales ACC does, it has a tough time converting those sales into profits (Net Income) and ultimately pass on those profits to the shareholders (EPS). So either ACC is operating in a bad sector or the company is not being managed properly.

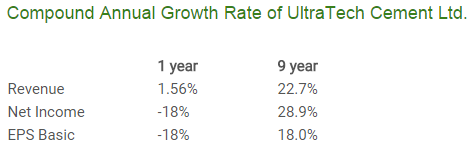

To see if ACC is operating in a bad sector, let us look at another cement stock, UltraTech Cement

UltraTech Cement’s revenue growth is much better than ACC. It was able to lower its expenses which is why the Net Income growth is better than Revenue growth. The EPS growth rate lower than the Net Income growth rate because UltraTech issued new stock for an acquisition.

By comparing these figures from two companies you should be able to figure out that the cement sector is not a bad sector to invest. Its just that ACC is not being managed well. It makes sense to invest in UltraTech Cement(not at current valuation though) instead of ACC.

Now and only now you can look at the company’s stock price to see if our analysis was right and to see how the market has valued ACC historically.

If you look at ACC’s share price from 31-March 2006 till 16-Jan-2015, its compound growth rate was 8.6%, which is not good. If you look at UltraTech Cement’s stock performance for the similar period, its growth rate was 22% which is fantastic. So our analysis about ACC was correct. The market agrees with our analysis, even rest of the market thinks that ACC is not a good company to invest which is why it has given such poor returns compared to UltraTech which has given fantastic returns.

In the long run the share price performance matches the company’s performance. We hope by now our members would understand why it so crucial to look at a company’s long term growth rates. You simply cannot ignore it.